|

ILIAS

eassessment Revision 61809

|

|

ILIAS

eassessment Revision 61809

|

Collaboration diagram for PHPExcel_Calculation_Financial:

Collaboration diagram for PHPExcel_Calculation_Financial:Static Public Member Functions | |

| static | ACCRINT ($issue, $firstinter, $settlement, $rate, $par=1000, $frequency=1, $basis=0) |

| ACCRINT. | |

| static | ACCRINTM ($issue, $settlement, $rate, $par=1000, $basis=0) |

| ACCRINTM. | |

| static | AMORDEGRC ($cost, $purchased, $firstPeriod, $salvage, $period, $rate, $basis=0) |

| static | AMORLINC ($cost, $purchased, $firstPeriod, $salvage, $period, $rate, $basis=0) |

| static | COUPDAYBS ($settlement, $maturity, $frequency, $basis=0) |

| static | COUPDAYS ($settlement, $maturity, $frequency, $basis=0) |

| static | COUPDAYSNC ($settlement, $maturity, $frequency, $basis=0) |

| static | COUPNCD ($settlement, $maturity, $frequency, $basis=0) |

| static | COUPNUM ($settlement, $maturity, $frequency, $basis=0) |

| static | COUPPCD ($settlement, $maturity, $frequency, $basis=0) |

| static | CUMIPMT ($rate, $nper, $pv, $start, $end, $type=0) |

| CUMIPMT. | |

| static | CUMPRINC ($rate, $nper, $pv, $start, $end, $type=0) |

| CUMPRINC. | |

| static | DB ($cost, $salvage, $life, $period, $month=12) |

| DB. | |

| static | DDB ($cost, $salvage, $life, $period, $factor=2.0) |

| DDB. | |

| static | DISC ($settlement, $maturity, $price, $redemption, $basis=0) |

| DISC. | |

| static | DOLLARDE ($fractional_dollar=Null, $fraction=0) |

| DOLLARDE. | |

| static | DOLLARFR ($decimal_dollar=Null, $fraction=0) |

| DOLLARFR. | |

| static | EFFECT ($nominal_rate=0, $npery=0) |

| EFFECT. | |

| static | FV ($rate=0, $nper=0, $pmt=0, $pv=0, $type=0) |

| FV. | |

| static | FVSCHEDULE ($principal, $schedule) |

| FVSCHEDULE. | |

| static | INTRATE ($settlement, $maturity, $investment, $redemption, $basis=0) |

| INTRATE. | |

| static | IPMT ($rate, $per, $nper, $pv, $fv=0, $type=0) |

| IPMT. | |

| static | IRR ($values, $guess=0.1) |

| static | ISPMT () |

| ISPMT. | |

| static | MIRR ($values, $finance_rate, $reinvestment_rate) |

| static | NOMINAL ($effect_rate=0, $npery=0) |

| NOMINAL. | |

| static | NPER ($rate=0, $pmt=0, $pv=0, $fv=0, $type=0) |

| NPER. | |

| static | NPV () |

| NPV. | |

| static | PMT ($rate=0, $nper=0, $pv=0, $fv=0, $type=0) |

| PMT. | |

| static | PPMT ($rate, $per, $nper, $pv, $fv=0, $type=0) |

| PPMT. | |

| static | PRICE ($settlement, $maturity, $rate, $yield, $redemption, $frequency, $basis=0) |

| static | PRICEDISC ($settlement, $maturity, $discount, $redemption, $basis=0) |

| PRICEDISC. | |

| static | PRICEMAT ($settlement, $maturity, $issue, $rate, $yield, $basis=0) |

| PRICEMAT. | |

| static | PV ($rate=0, $nper=0, $pmt=0, $fv=0, $type=0) |

| PV. | |

| static | RATE ($nper, $pmt, $pv, $fv=0.0, $type=0, $guess=0.1) |

| RATE. | |

| static | RECEIVED ($settlement, $maturity, $investment, $discount, $basis=0) |

| RECEIVED. | |

| static | SLN ($cost, $salvage, $life) |

| SLN. | |

| static | SYD ($cost, $salvage, $life, $period) |

| SYD. | |

| static | TBILLEQ ($settlement, $maturity, $discount) |

| TBILLEQ. | |

| static | TBILLPRICE ($settlement, $maturity, $discount) |

| TBILLPRICE. | |

| static | TBILLYIELD ($settlement, $maturity, $price) |

| TBILLYIELD. | |

| static | XIRR ($values, $dates, $guess=0.1) |

| static | XNPV ($rate, $values, $dates) |

| XNPV. | |

| static | YIELDDISC ($settlement, $maturity, $price, $redemption, $basis=0) |

| YIELDDISC. | |

| static | YIELDMAT ($settlement, $maturity, $issue, $rate, $price, $basis=0) |

| YIELDMAT. | |

Static Private Member Functions | |

| static | _lastDayOfMonth ($testDate) |

| static | _firstDayOfMonth ($testDate) |

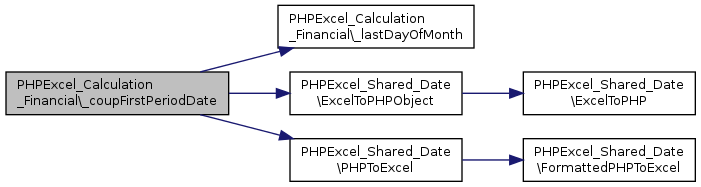

| static | _coupFirstPeriodDate ($settlement, $maturity, $frequency, $next) |

| static | _validFrequency ($frequency) |

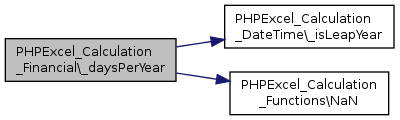

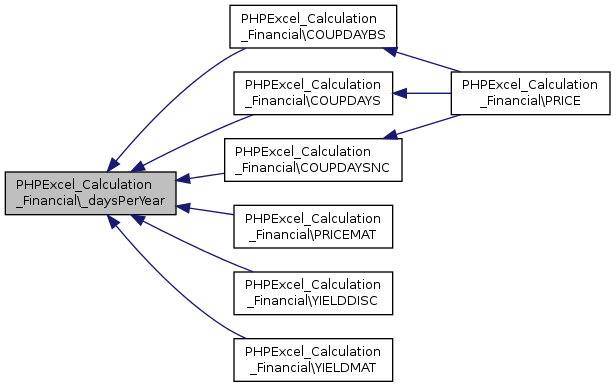

| static | _daysPerYear ($year, $basis) |

| static | _interestAndPrincipal ($rate=0, $per=0, $nper=0, $pv=0, $fv=0, $type=0) |

Definition at line 53 of file Financial.php.

|

staticprivate |

Definition at line 68 of file Financial.php.

References _lastDayOfMonth(), PHPExcel_Shared_Date\ExcelToPHPObject(), and PHPExcel_Shared_Date\PHPToExcel().

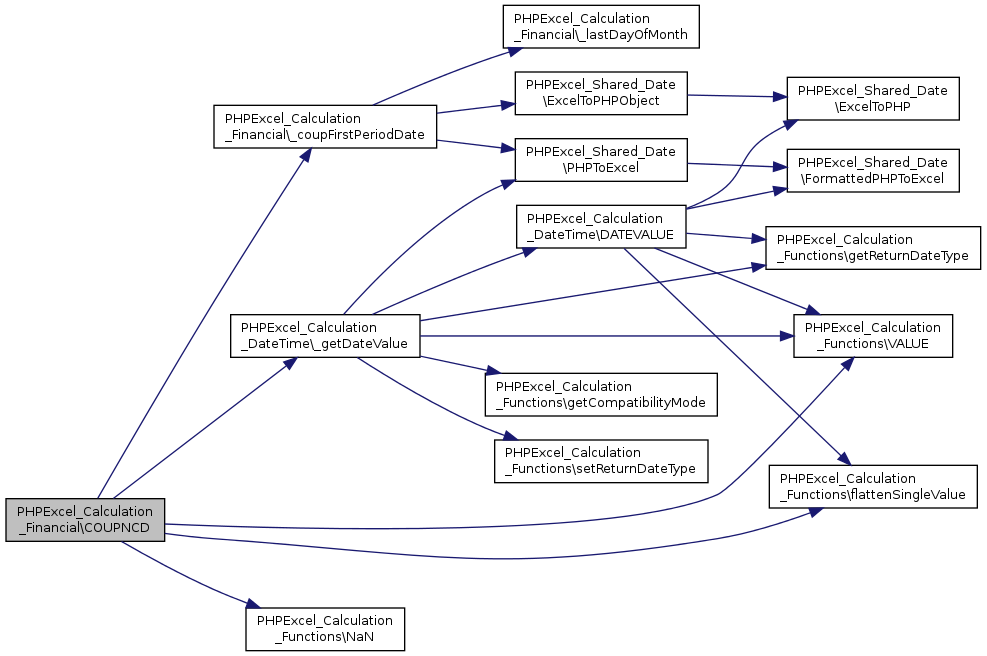

Referenced by COUPDAYBS(), COUPDAYS(), COUPDAYSNC(), COUPNCD(), COUPNUM(), and COUPPCD().

Here is the call graph for this function: Here is the caller graph for this function:

|

staticprivate |

Definition at line 101 of file Financial.php.

References PHPExcel_Calculation_DateTime\_isLeapYear(), and PHPExcel_Calculation_Functions\NaN().

Referenced by COUPDAYBS(), COUPDAYS(), COUPDAYSNC(), PRICEMAT(), YIELDDISC(), and YIELDMAT().

Here is the call graph for this function: Here is the caller graph for this function:

|

staticprivate |

Definition at line 62 of file Financial.php.

|

staticprivate |

Definition at line 125 of file Financial.php.

Referenced by IPMT(), and PPMT().

Here is the call graph for this function: Here is the caller graph for this function:

|

staticprivate |

Definition at line 55 of file Financial.php.

Referenced by _coupFirstPeriodDate().

Here is the caller graph for this function:

|

staticprivate |

Definition at line 89 of file Financial.php.

References PHPExcel_Calculation_Functions\COMPATIBILITY_GNUMERIC, and PHPExcel_Calculation_Functions\getCompatibilityMode().

Here is the call graph for this function:

|

static |

ACCRINT.

Returns the discount rate for a security.

| mixed | issue The security's issue date. |

| mixed | firstinter The security's first interest date. |

| mixed | settlement The security's settlement date. |

| float | rate The security's annual coupon rate. |

| float | par The security's par value. |

| int | basis The type of day count to use. 0 or omitted US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 |

Definition at line 155 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

static |

ACCRINTM.

Returns the discount rate for a security.

| mixed | issue The security's issue date. |

| mixed | settlement The security's settlement date. |

| float | rate The security's annual coupon rate. |

| float | par The security's par value. |

| int | basis The type of day count to use. 0 or omitted US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 |

Definition at line 198 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

static |

Definition at line 221 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

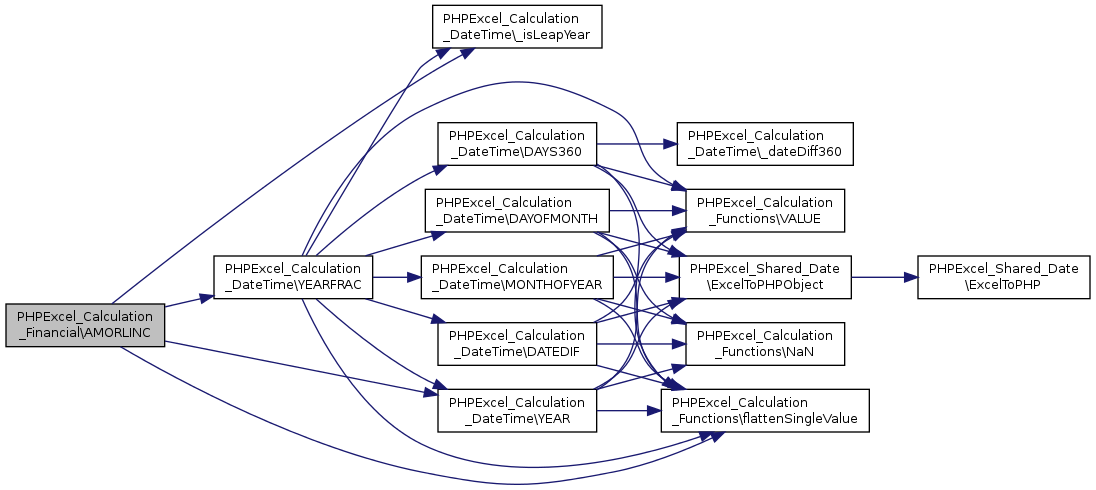

static |

Definition at line 266 of file Financial.php.

References PHPExcel_Calculation_DateTime\_isLeapYear(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_DateTime\YEAR(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

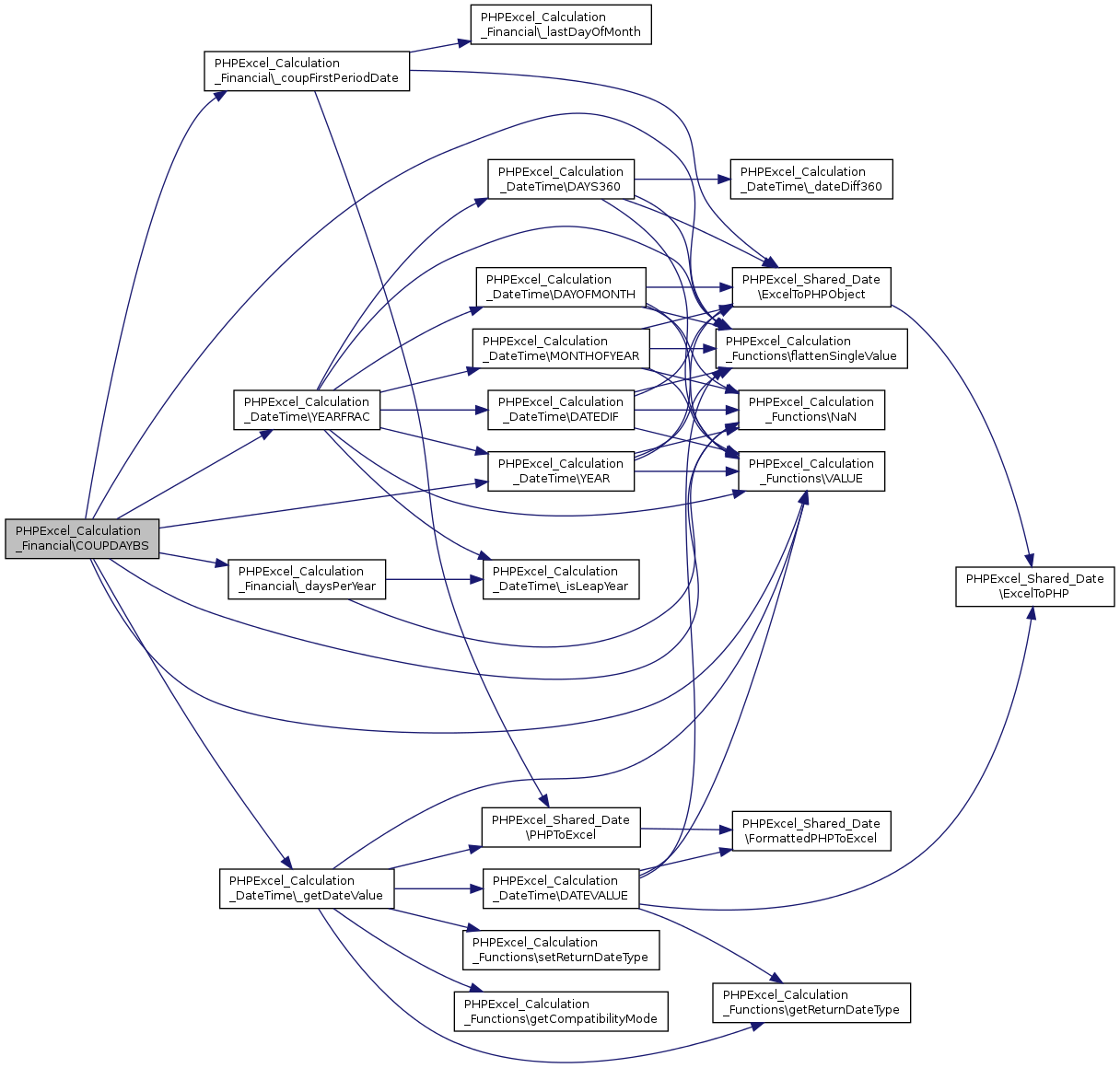

static |

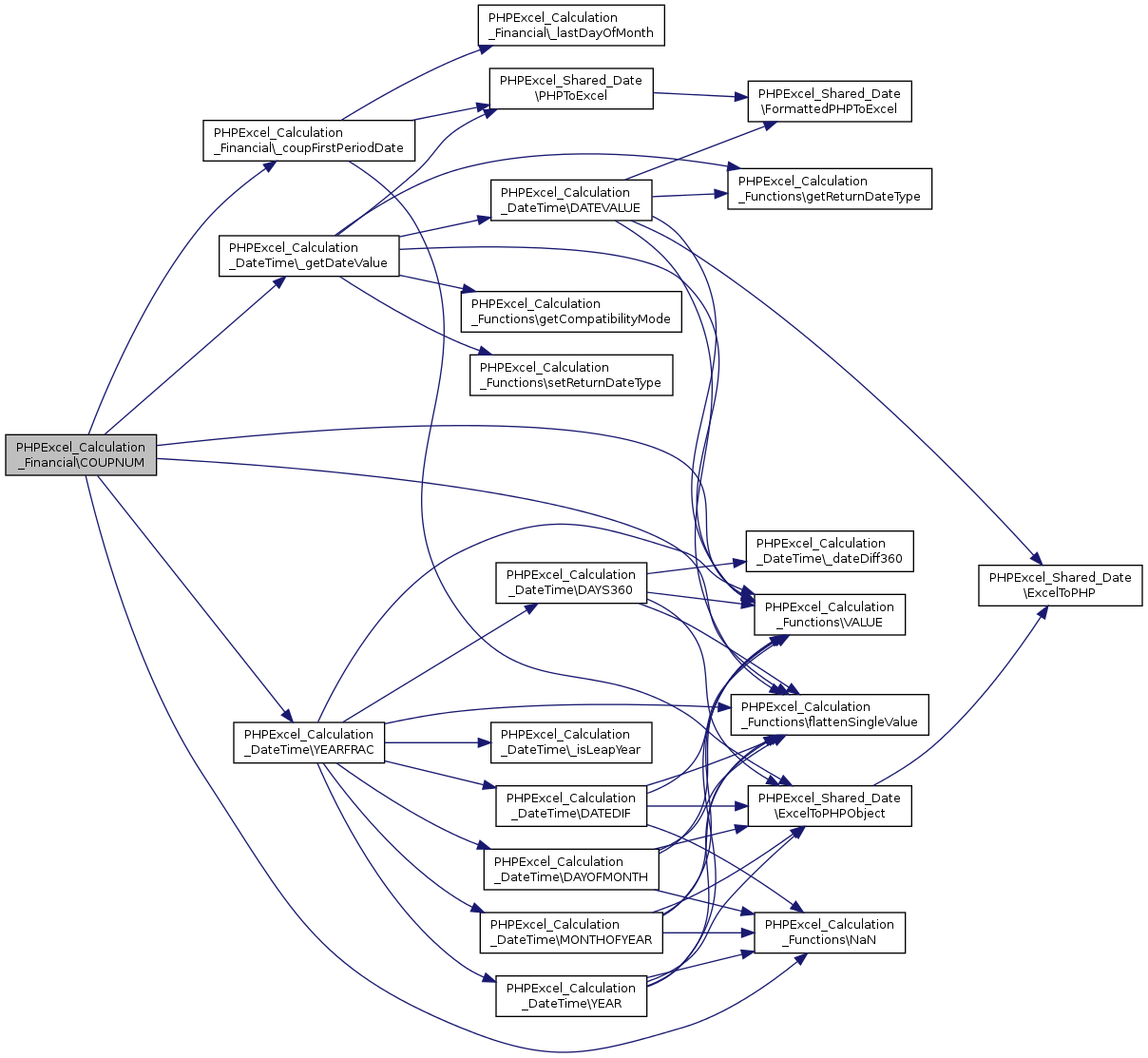

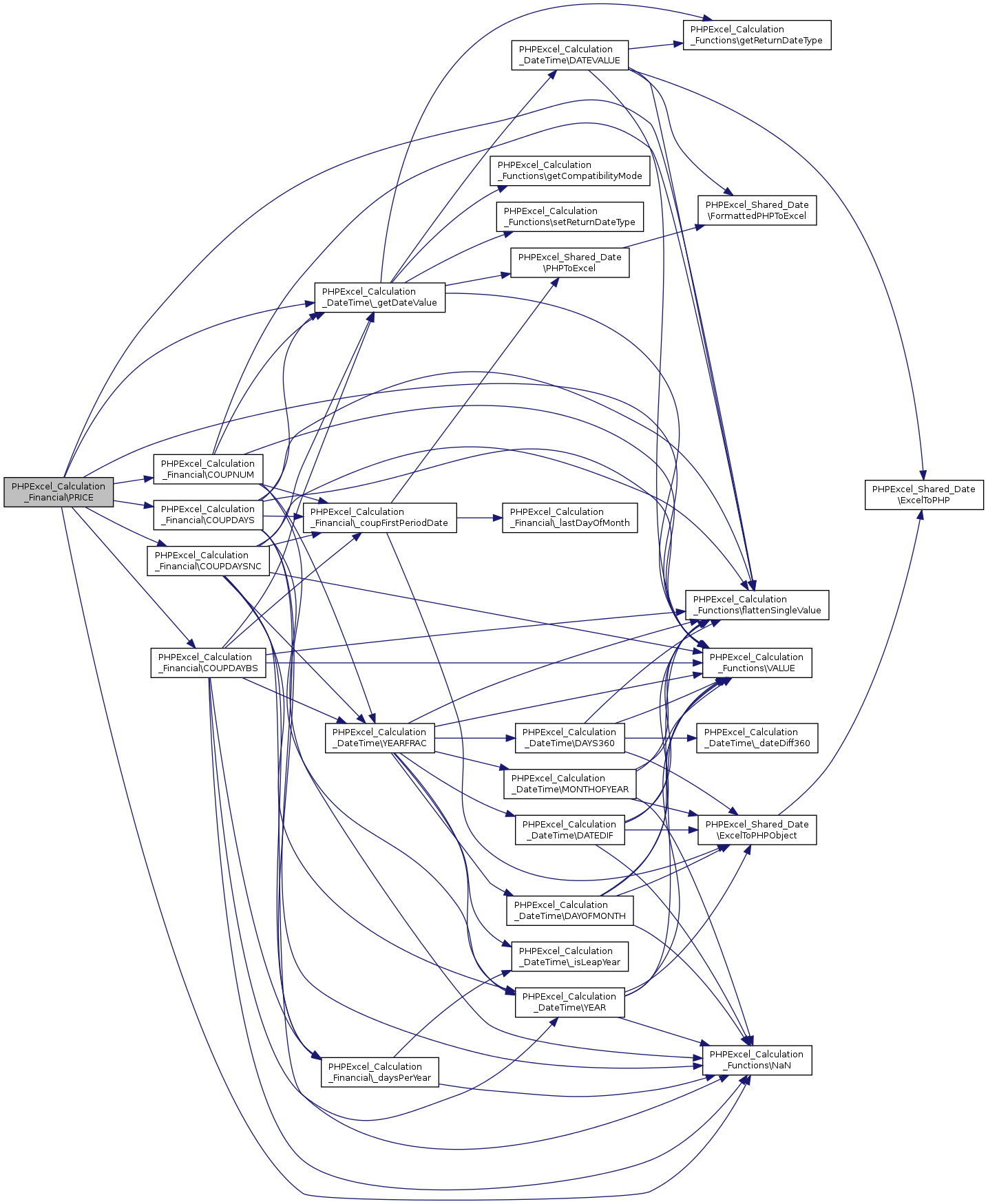

Definition at line 300 of file Financial.php.

References _coupFirstPeriodDate(), _daysPerYear(), PHPExcel_Calculation_DateTime\_getDateValue(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), PHPExcel_Calculation_DateTime\YEAR(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Referenced by PRICE().

Here is the call graph for this function: Here is the caller graph for this function:

|

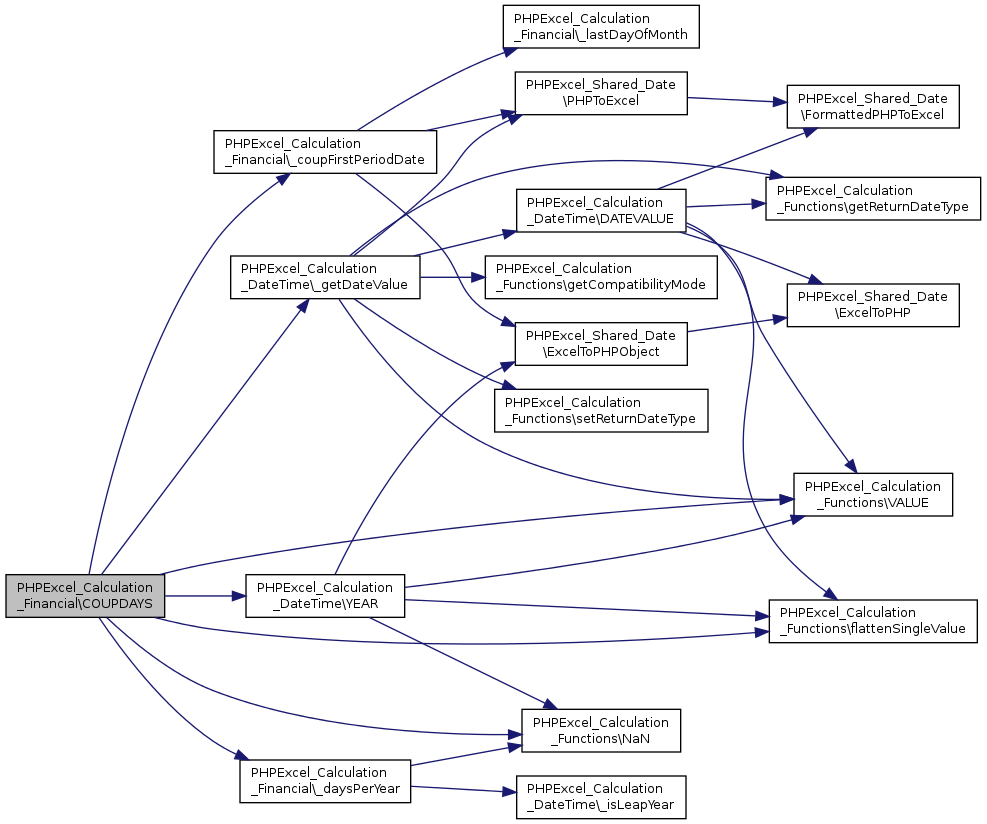

static |

Definition at line 326 of file Financial.php.

References _coupFirstPeriodDate(), _daysPerYear(), PHPExcel_Calculation_DateTime\_getDateValue(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEAR().

Referenced by PRICE().

Here is the call graph for this function: Here is the caller graph for this function:

|

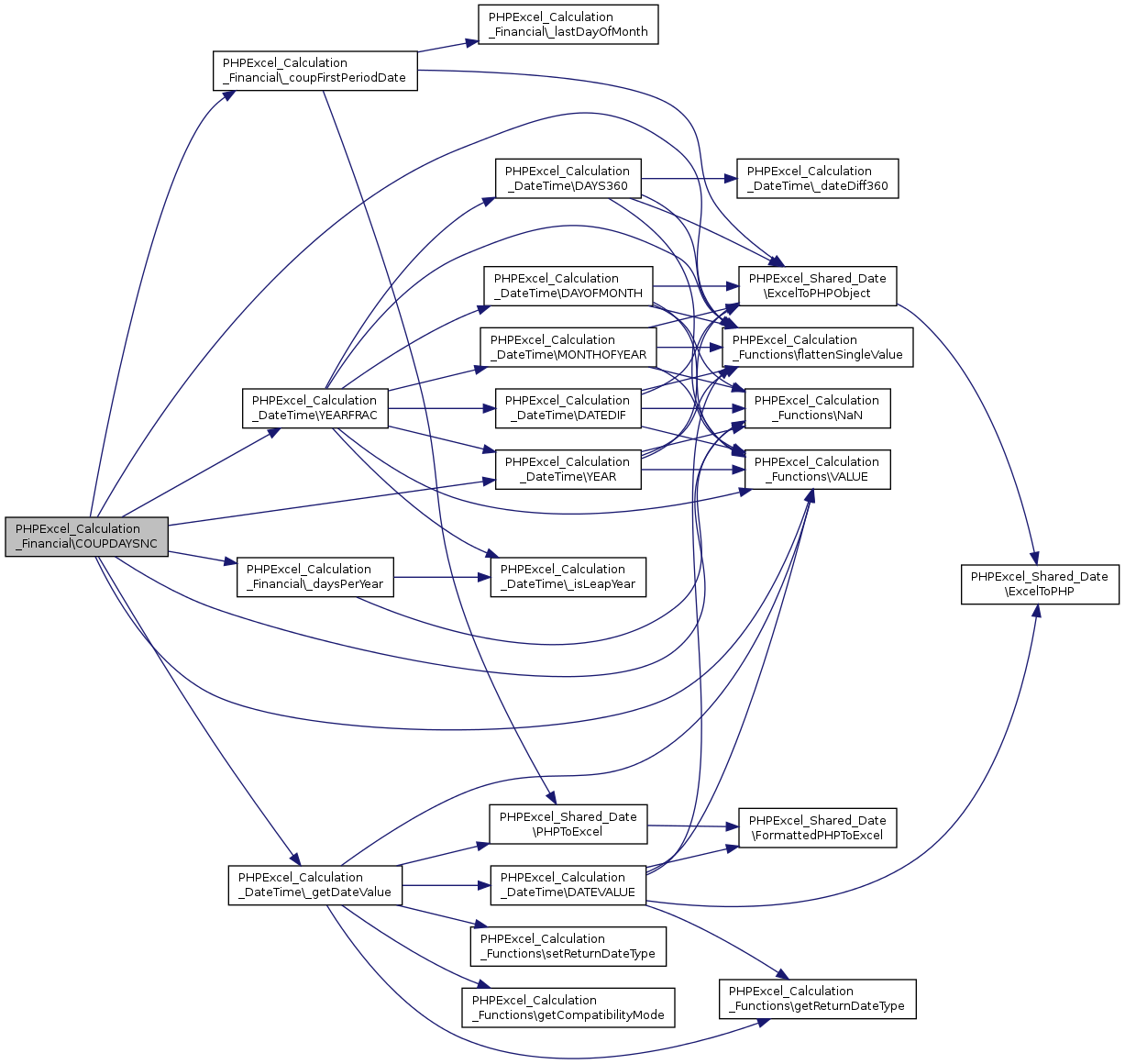

static |

Definition at line 364 of file Financial.php.

References _coupFirstPeriodDate(), _daysPerYear(), PHPExcel_Calculation_DateTime\_getDateValue(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), PHPExcel_Calculation_DateTime\YEAR(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Referenced by PRICE().

Here is the call graph for this function: Here is the caller graph for this function:

|

static |

Definition at line 390 of file Financial.php.

References _coupFirstPeriodDate(), PHPExcel_Calculation_DateTime\_getDateValue(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

static |

Definition at line 413 of file Financial.php.

References _coupFirstPeriodDate(), PHPExcel_Calculation_DateTime\_getDateValue(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Referenced by PRICE().

Here is the call graph for this function: Here is the caller graph for this function:

|

static |

Definition at line 451 of file Financial.php.

References _coupFirstPeriodDate(), PHPExcel_Calculation_DateTime\_getDateValue(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

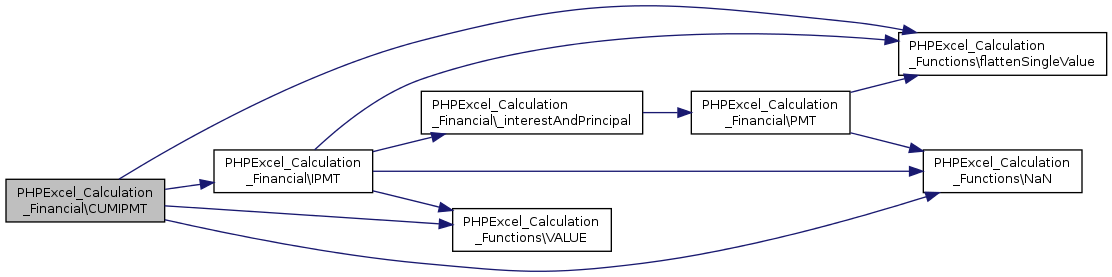

static |

CUMIPMT.

Returns the cumulative interest paid on a loan between start_period and end_period.

| float | $rate | Interest rate per period |

| int | $nper | Number of periods |

| float | $pv | Present Value |

| int | start The first period in the calculation. Payment periods are numbered beginning with 1. | |

| int | end The last period in the calculation. | |

| int | $type | Payment type: 0 = at the end of each period, 1 = at the beginning of each period |

Definition at line 488 of file Financial.php.

References $type, PHPExcel_Calculation_Functions\flattenSingleValue(), IPMT(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

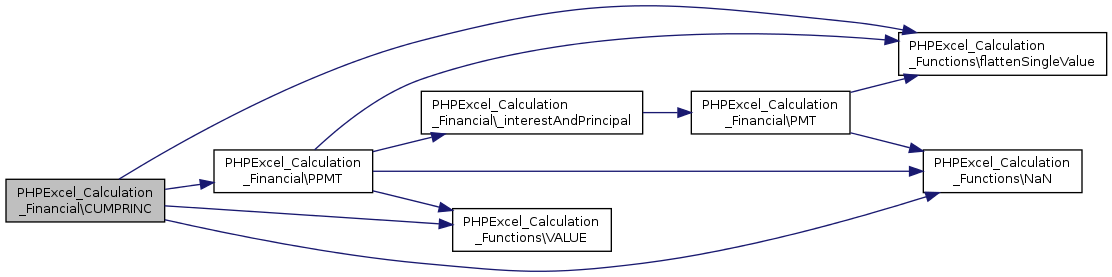

static |

CUMPRINC.

Returns the cumulative principal paid on a loan between start_period and end_period.

| float | $rate | Interest rate per period |

| int | $nper | Number of periods |

| float | $pv | Present Value |

| int | start The first period in the calculation. Payment periods are numbered beginning with 1. | |

| int | end The last period in the calculation. | |

| int | $type | Payment type: 0 = at the end of each period, 1 = at the beginning of each period |

Definition at line 528 of file Financial.php.

References $type, PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PPMT(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

static |

DB.

Returns the depreciation of an asset for a specified period using the fixed-declining balance method. This form of depreciation is used if you want to get a higher depreciation value at the beginning of the depreciation (as opposed to linear depreciation). The depreciation value is reduced with every depreciation period by the depreciation already deducted from the initial cost.

| float | cost Initial cost of the asset. |

| float | salvage Value at the end of the depreciation. (Sometimes called the salvage value of the asset) |

| int | life Number of periods over which the asset is depreciated. (Sometimes called the useful life of the asset) |

| int | period The period for which you want to calculate the depreciation. Period must use the same units as life. |

| float | month Number of months in the first year. If month is omitted, it defaults to 12. |

Definition at line 569 of file Financial.php.

References PHPExcel_Calculation_Functions\COMPATIBILITY_GNUMERIC, PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\getCompatibilityMode(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

static |

DDB.

Returns the depreciation of an asset for a specified period using the double-declining balance method or some other method you specify.

| float | cost Initial cost of the asset. |

| float | salvage Value at the end of the depreciation. (Sometimes called the salvage value of the asset) |

| int | life Number of periods over which the asset is depreciated. (Sometimes called the useful life of the asset) |

| int | period The period for which you want to calculate the depreciation. Period must use the same units as life. |

| float | factor The rate at which the balance declines. If factor is omitted, it is assumed to be 2 (the double-declining balance method). |

Definition at line 621 of file Financial.php.

References PHPExcel_Calculation_Functions\COMPATIBILITY_GNUMERIC, PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\getCompatibilityMode(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

static |

DISC.

Returns the discount rate for a security.

| mixed | settlement The security's settlement date. The security settlement date is the date after the issue date when the security is traded to the buyer. |

| mixed | maturity The security's maturity date. The maturity date is the date when the security expires. |

| int | price The security's price per $100 face value. |

| int | redemption the security's redemption value per $100 face value. |

| int | basis The type of day count to use. 0 or omitted US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 |

Definition at line 671 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

static |

DOLLARDE.

Converts a dollar price expressed as an integer part and a fraction part into a dollar price expressed as a decimal number. Fractional dollar numbers are sometimes used for security prices.

| float | $fractional_dollar | Fractional Dollar |

| int | $fraction | Fraction |

Definition at line 705 of file Financial.php.

References PHPExcel_Calculation_Functions\DIV0(), PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_Functions\NaN().

Here is the call graph for this function:

|

static |

DOLLARFR.

Converts a dollar price expressed as a decimal number into a dollar price expressed as a fraction. Fractional dollar numbers are sometimes used for security prices.

| float | $decimal_dollar | Decimal Dollar |

| int | $fraction | Fraction |

Definition at line 735 of file Financial.php.

References PHPExcel_Calculation_Functions\DIV0(), PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_Functions\NaN().

Here is the call graph for this function:

|

static |

EFFECT.

Returns the effective interest rate given the nominal rate and the number of compounding payments per year.

| float | $nominal_rate | Nominal interest rate |

| int | $npery | Number of compounding payments per year |

Definition at line 764 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_Functions\NaN().

Here is the call graph for this function:

|

static |

FV.

Returns the Future Value of a cash flow with constant payments and interest rate (annuities).

| float | $rate | Interest rate per period |

| int | $nper | Number of periods |

| float | $pmt | Periodic payment (annuity) |

| float | $pv | Present Value |

| int | $type | Payment type: 0 = at the end of each period, 1 = at the beginning of each period |

Definition at line 789 of file Financial.php.

References $type, PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_Functions\NaN().

Here is the call graph for this function:

|

static |

FVSCHEDULE.

Definition at line 814 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenArray(), and PHPExcel_Calculation_Functions\flattenSingleValue().

Here is the call graph for this function:

|

static |

INTRATE.

Returns the interest rate for a fully invested security.

| mixed | settlement The security's settlement date. The security settlement date is the date after the issue date when the security is traded to the buyer. |

| mixed | maturity The security's maturity date. The maturity date is the date when the security expires. |

| int | investment The amount invested in the security. |

| int | redemption The amount to be received at maturity. |

| int | basis The type of day count to use. 0 or omitted US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 |

Definition at line 845 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

static |

IPMT.

Returns the interest payment for a given period for an investment based on periodic, constant payments and a constant interest rate.

| float | $rate | Interest rate per period |

| int | $per | Period for which we want to find the interest |

| int | $nper | Number of periods |

| float | $pv | Present Value |

| float | $fv | Future Value |

| int | $type | Payment type: 0 = at the end of each period, 1 = at the beginning of each period |

Definition at line 882 of file Financial.php.

References $type, _interestAndPrincipal(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Referenced by CUMIPMT().

Here is the call graph for this function: Here is the caller graph for this function:

|

static |

Definition at line 904 of file Financial.php.

References $f, FINANCIAL_MAX_ITERATIONS, FINANCIAL_PRECISION, PHPExcel_Calculation_Functions\flattenArray(), PHPExcel_Calculation_Functions\flattenSingleValue(), NPV(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

static |

ISPMT.

Returns the interest payment for an investment based on an interest rate and a constant payment schedule.

Excel Function: =ISPMT(interest_rate, period, number_payments, PV)

interest_rate is the interest rate for the investment

period is the period to calculate the interest rate. It must be betweeen 1 and number_payments.

number_payments is the number of payments for the annuity

PV is the loan amount or present value of the payments

Definition at line 960 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenArray().

Here is the call graph for this function:

|

static |

Definition at line 985 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenArray(), PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

static |

NOMINAL.

Returns the nominal interest rate given the effective rate and the number of compounding payments per year.

| float | $effect_rate | Effective interest rate |

| int | $npery | Number of compounding payments per year |

Definition at line 1024 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_Functions\NaN().

Here is the call graph for this function:

|

static |

NPER.

Returns the number of periods for a cash flow with constant periodic payments (annuities), and interest rate.

@param float $rate Interest rate per period @param int $pmt Periodic payment (annuity) @param float $pv Present Value @param float $fv Future Value @param int $type Payment type: 0 = at the end of each period, 1 = at the beginning of each period @return float

Definition at line 1050 of file Financial.php.

References $type, PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_Functions\NaN().

Here is the call graph for this function:

|

static |

NPV.

Returns the Net Present Value of a cash flow series given a discount rate.

| float | Discount interest rate |

| array | Cash flow series |

Definition at line 1086 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenArray().

Referenced by IRR().

Here is the call graph for this function: Here is the caller graph for this function:

|

static |

PMT.

Returns the constant payment (annuity) for a cash flow with a constant interest rate.

| float | $rate | Interest rate per period |

| int | $nper | Number of periods |

| float | $pv | Present Value |

| float | $fv | Future Value |

| int | $type | Payment type: 0 = at the end of each period, 1 = at the beginning of each period |

Definition at line 1119 of file Financial.php.

References $type, PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_Functions\NaN().

Referenced by _interestAndPrincipal().

Here is the call graph for this function: Here is the caller graph for this function:

|

static |

PPMT.

Returns the interest payment for a given period for an investment based on periodic, constant payments and a constant interest rate.

| float | $rate | Interest rate per period |

| int | $per | Period for which we want to find the interest |

| int | $nper | Number of periods |

| float | $pv | Present Value |

| float | $fv | Future Value |

| int | $type | Payment type: 0 = at the end of each period, 1 = at the beginning of each period |

Definition at line 1153 of file Financial.php.

References $type, _interestAndPrincipal(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Referenced by CUMPRINC().

Here is the call graph for this function: Here is the caller graph for this function:

|

static |

Definition at line 1175 of file Financial.php.

References PHPExcel_Calculation_DateTime\_getDateValue(), COUPDAYBS(), COUPDAYS(), COUPDAYSNC(), COUPNUM(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

static |

PRICEDISC.

Returns the price per $100 face value of a discounted security.

| mixed | settlement The security's settlement date. The security settlement date is the date after the issue date when the security is traded to the buyer. |

| mixed | maturity The security's maturity date. The maturity date is the date when the security expires. |

| int | discount The security's discount rate. |

| int | redemption The security's redemption value per $100 face value. |

| int | basis The type of day count to use. 0 or omitted US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 |

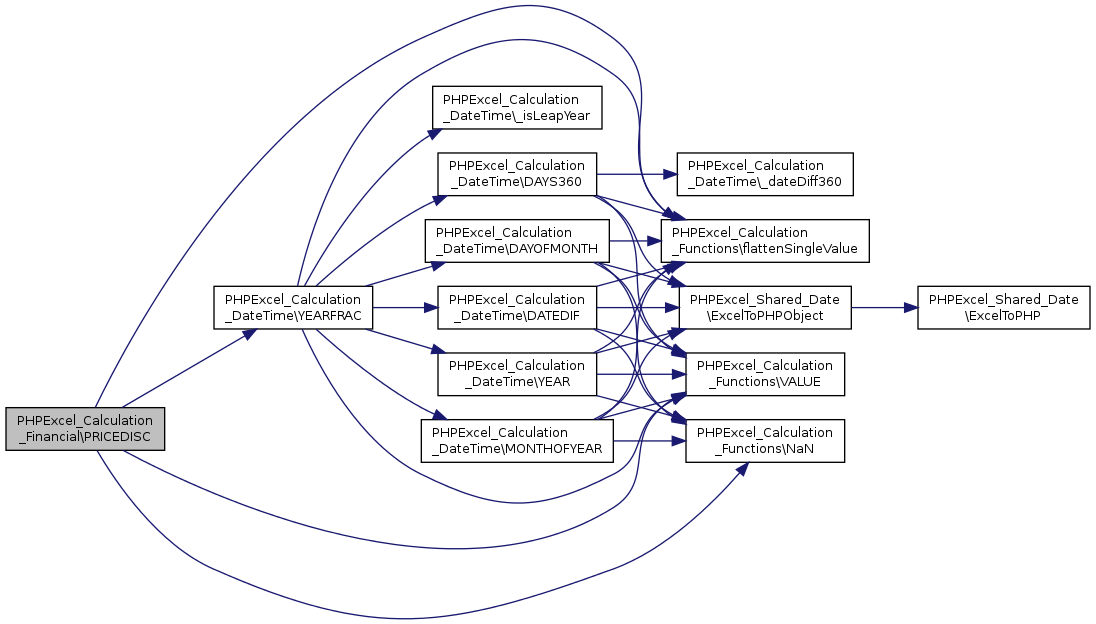

Definition at line 1235 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

static |

PRICEMAT.

Returns the price per $100 face value of a security that pays interest at maturity.

| mixed | settlement The security's settlement date. The security's settlement date is the date after the issue date when the security is traded to the buyer. |

| mixed | maturity The security's maturity date. The maturity date is the date when the security expires. |

| mixed | issue The security's issue date. |

| int | rate The security's interest rate at date of issue. |

| int | yield The security's annual yield. |

| int | basis The type of day count to use. 0 or omitted US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 |

Definition at line 1279 of file Financial.php.

References _daysPerYear(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), PHPExcel_Calculation_DateTime\YEAR(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

static |

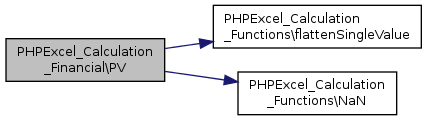

PV.

Returns the Present Value of a cash flow with constant payments and interest rate (annuities).

| float | $rate | Interest rate per period |

| int | $nper | Number of periods |

| float | $pmt | Periodic payment (annuity) |

| float | $fv | Future Value |

| int | $type | Payment type: 0 = at the end of each period, 1 = at the beginning of each period |

Definition at line 1335 of file Financial.php.

References $type, PHPExcel_Calculation_Functions\flattenSingleValue(), and PHPExcel_Calculation_Functions\NaN().

Here is the call graph for this function:

|

static |

RATE.

Definition at line 1360 of file Financial.php.

References $f, $type, $y, FINANCIAL_MAX_ITERATIONS, FINANCIAL_PRECISION, and PHPExcel_Calculation_Functions\flattenSingleValue().

Here is the call graph for this function:

|

static |

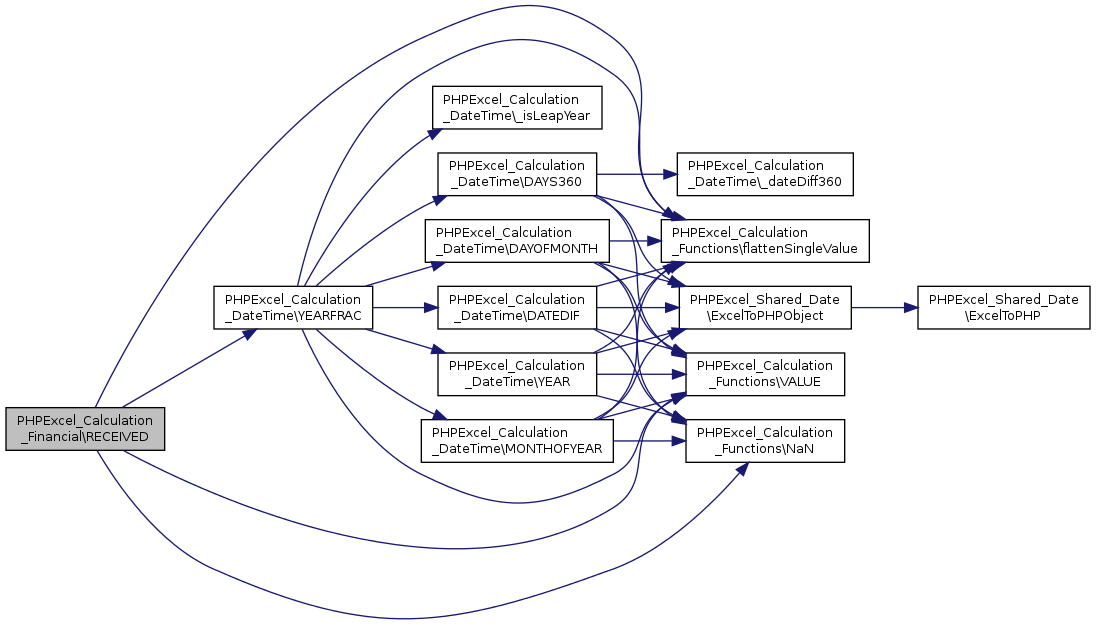

RECEIVED.

Returns the price per $100 face value of a discounted security.

| mixed | settlement The security's settlement date. The security settlement date is the date after the issue date when the security is traded to the buyer. |

| mixed | maturity The security's maturity date. The maturity date is the date when the security expires. |

| int | investment The amount invested in the security. |

| int | discount The security's discount rate. |

| int | basis The type of day count to use. 0 or omitted US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 |

Definition at line 1420 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

static |

SLN.

Returns the straight-line depreciation of an asset for one period

| cost | Initial cost of the asset |

| salvage | Value at the end of the depreciation |

| life | Number of periods over which the asset is depreciated |

Definition at line 1454 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

static |

SYD.

Returns the sum-of-years' digits depreciation of an asset for a specified period.

| cost | Initial cost of the asset |

| salvage | Value at the end of the depreciation |

| life | Number of periods over which the asset is depreciated |

| period | Period |

Definition at line 1481 of file Financial.php.

References PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Here is the call graph for this function:

|

static |

TBILLEQ.

Returns the bond-equivalent yield for a Treasury bill.

| mixed | settlement The Treasury bill's settlement date. The Treasury bill's settlement date is the date after the issue date when the Treasury bill is traded to the buyer. |

| mixed | maturity The Treasury bill's maturity date. The maturity date is the date when the Treasury bill expires. |

| int | discount The Treasury bill's discount rate. |

Definition at line 1510 of file Financial.php.

References PHPExcel_Calculation_DateTime\_getDateValue(), PHPExcel_Calculation_Functions\COMPATIBILITY_OPENOFFICE, PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\getCompatibilityMode(), TBILLPRICE(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

static |

TBILLPRICE.

Returns the yield for a Treasury bill.

| mixed | settlement The Treasury bill's settlement date. The Treasury bill's settlement date is the date after the issue date when the Treasury bill is traded to the buyer. |

| mixed | maturity The Treasury bill's maturity date. The maturity date is the date when the Treasury bill expires. |

| int | discount The Treasury bill's discount rate. |

Definition at line 1548 of file Financial.php.

References PHPExcel_Calculation_DateTime\_getDateValue(), PHPExcel_Calculation_Functions\COMPATIBILITY_OPENOFFICE, PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\getCompatibilityMode(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Referenced by TBILLEQ().

Here is the call graph for this function: Here is the caller graph for this function:

|

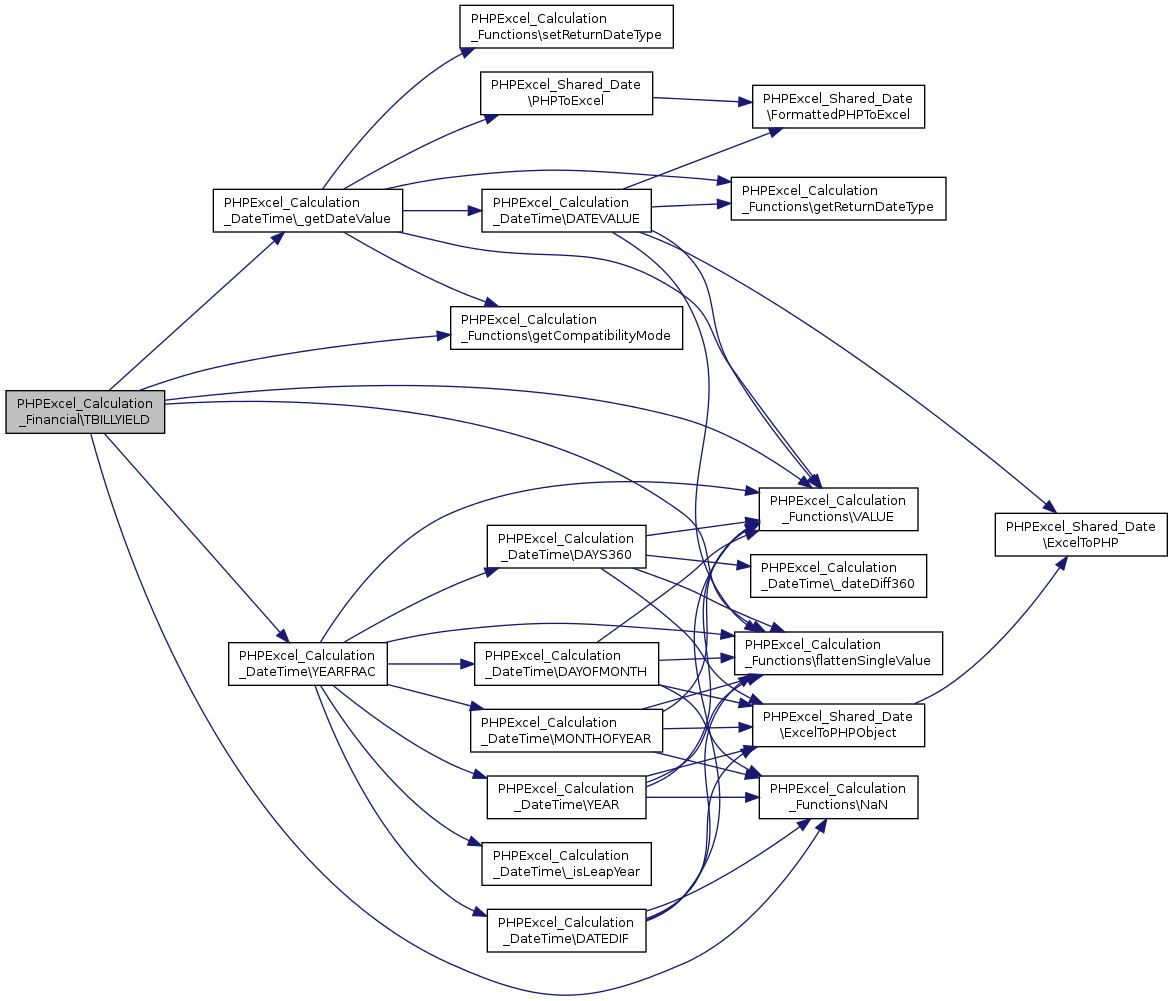

static |

TBILLYIELD.

Returns the yield for a Treasury bill.

| mixed | settlement The Treasury bill's settlement date. The Treasury bill's settlement date is the date after the issue date when the Treasury bill is traded to the buyer. |

| mixed | maturity The Treasury bill's maturity date. The maturity date is the date when the Treasury bill expires. |

| int | price The Treasury bill's price per $100 face value. |

Definition at line 1600 of file Financial.php.

References PHPExcel_Calculation_DateTime\_getDateValue(), PHPExcel_Calculation_Functions\COMPATIBILITY_OPENOFFICE, PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\getCompatibilityMode(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

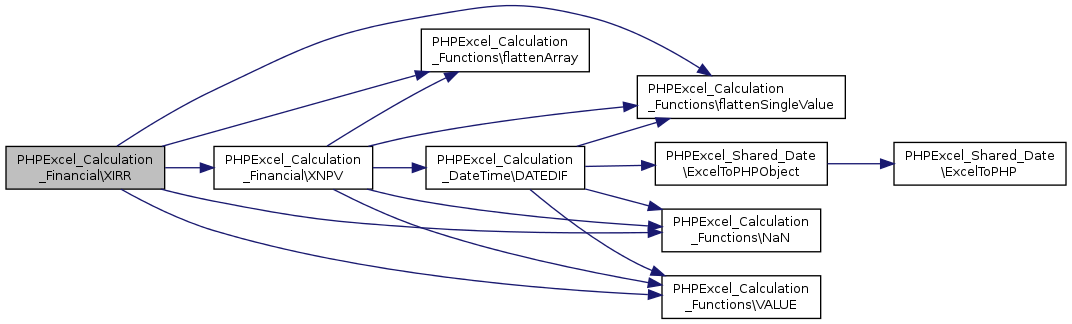

static |

Definition at line 1632 of file Financial.php.

References $f, FINANCIAL_MAX_ITERATIONS, FINANCIAL_PRECISION, PHPExcel_Calculation_Functions\flattenArray(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), and XNPV().

Here is the call graph for this function:

|

static |

XNPV.

Returns the net present value for a schedule of cash flows that is not necessarily periodic. To calculate the net present value for a series of cash flows that is periodic, use the NPV function.

Excel Function: =XNPV(rate,values,dates)

| float | $rate | The discount rate to apply to the cash flows. |

| array | of float $values A series of cash flows that corresponds to a schedule of payments in dates. The first payment is optional and corresponds to a cost or payment that occurs at the beginning of the investment. If the first value is a cost or payment, it must be a negative value. All succeeding payments are discounted based on a 365-day year. The series of values must contain at least one positive value and one negative value. | |

| array | of mixed $dates A schedule of payment dates that corresponds to the cash flow payments. The first payment date indicates the beginning of the schedule of payments. All other dates must be later than this date, but they may occur in any order. |

Definition at line 1688 of file Financial.php.

References PHPExcel_Calculation_DateTime\DATEDIF(), PHPExcel_Calculation_Functions\flattenArray(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), and PHPExcel_Calculation_Functions\VALUE().

Referenced by XIRR().

Here is the call graph for this function: Here is the caller graph for this function:

|

static |

YIELDDISC.

Returns the annual yield of a security that pays interest at maturity.

| mixed | settlement The security's settlement date. The security's settlement date is the date after the issue date when the security is traded to the buyer. |

| mixed | maturity The security's maturity date. The maturity date is the date when the security expires. |

| int | price The security's price per $100 face value. |

| int | redemption The security's redemption value per $100 face value. |

| int | basis The type of day count to use. 0 or omitted US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 |

Definition at line 1726 of file Financial.php.

References _daysPerYear(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), PHPExcel_Calculation_DateTime\YEAR(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function:

|

static |

YIELDMAT.

Returns the annual yield of a security that pays interest at maturity.

| mixed | settlement The security's settlement date. The security's settlement date is the date after the issue date when the security is traded to the buyer. |

| mixed | maturity The security's maturity date. The maturity date is the date when the security expires. |

| mixed | issue The security's issue date. |

| int | rate The security's interest rate at date of issue. |

| int | price The security's price per $100 face value. |

| int | basis The type of day count to use. 0 or omitted US (NASD) 30/360 1 Actual/actual 2 Actual/360 3 Actual/365 4 European 30/360 |

Definition at line 1775 of file Financial.php.

References _daysPerYear(), PHPExcel_Calculation_Functions\flattenSingleValue(), PHPExcel_Calculation_Functions\NaN(), PHPExcel_Calculation_Functions\VALUE(), PHPExcel_Calculation_DateTime\YEAR(), and PHPExcel_Calculation_DateTime\YEARFRAC().

Here is the call graph for this function: 1.8.1.2 (using Doxyfile)

1.8.1.2 (using Doxyfile)